Home Loan vs Personal Loan: Which Should You Choose in India?

When you require a substantial amount of money, whether it is for purchasing a house, home renovation, or meeting a large expense, the choice between two available options often boils down to two: home loan and personal loan. While both options provide you with instant access to money, they are designed for entirely different purposes. In the india year 2026, when the interest rates are fluctuating and the budgets of households are under stress, making the wrong choice can prove costly, with lakhs of rupees going down the drain in the form of additional interest. This comprehensive guide compares home loan vs personal loan in simple terms, including cost, tenure, eligibility criteria, tax benefits, and practical examples, so that you can make the right choice according to your needs.

How This Guide Helps Indian Borrowers

This guide compares home loans and personal loans from the perspective of an Indian borrower. It highlights the cost, tax benefits, tenure, approval process, and practical applications so you can make the right decision for your financial needs.

What Is a Home Loan?

A home loan is a secured loan taken to:

- Buy a new house or flat

- Purchase a plot

- Construct a home

- Renovate or extend an existing house

The property acts as collateral. Because the bank has security, interest rates are lower and tenures are longer-often up to 30 years.

Typical features in 2026:

- Interest rate: 8%-10%

- Tenure: Up to 30 years

- Loan amount: Up to 75-90% of property value

What Is a Personal Loan?

A personal loan is an unsecured loan. You can use it for almost anything:

- Medical emergencies

- Weddings

- Travel

- Education

- Gadgets or appliances

- Debt consolidation

Since there’s no collateral, banks charge higher interest and offer shorter tenures.

Typical features in 2026:

- Interest rate: 11%-24%

- Tenure: 1-5 years

- Faster approval, minimal paperwork

Home Loan vs Personal Loan: Quick Comparison

| Feature | Home Loan | Personal Loan |

|---|---|---|

| Interest Rate | 8%-10% | 11%-24% |

| Tenure | Up to 30 years | 1-5 years |

| Collateral | Property | None |

| Loan Amount | High (in lakhs/crores) | Moderate |

| Processing Time | Slower | Fast |

| Tax Benefits | Available | None |

The difference in cost over time can be massive.

Cost Matters: How Much Extra Will You Pay?

Let’s compare ₹10 lakh over 10 years:

- Home Loan @ 9%

- EMI ≈ ₹12,700

- Total interest ≈ ₹5.2 lakh

- Personal Loan @ 15%

- EMI ≈ ₹16,100

- Total interest ≈ ₹9.3 lakh

That’s over ₹4 lakh more in interest with a personal loan.

For big, long-term needs, home loans are far cheaper.

Speed vs Savings: What Do You Value?

Personal loans win on speed:

- Online approval

- Minimal documents

- Disbursal in hours

Home loans take time:

- Property verification

- Legal checks

- Valuation

- Multiple approvals

But what you gain in speed with a personal loan, you lose in interest.

Ask yourself:

- Do I need money today?

- Or can I wait a few weeks to save lakhs?

When a Home Loan Makes Sense

Choose a home loan if:

- You are buying or building a house

- The amount is large

- You want lower EMIs

- You plan for long-term stability

- You want tax benefits

Home loans are designed for big life goals.

When a Personal Loan Is Better

Choose a personal loan if:

- The need is urgent

- The amount is small to medium

- You don’t want to pledge property

- The purpose isn’t housing-related

For short-term needs, personal loans are practical.

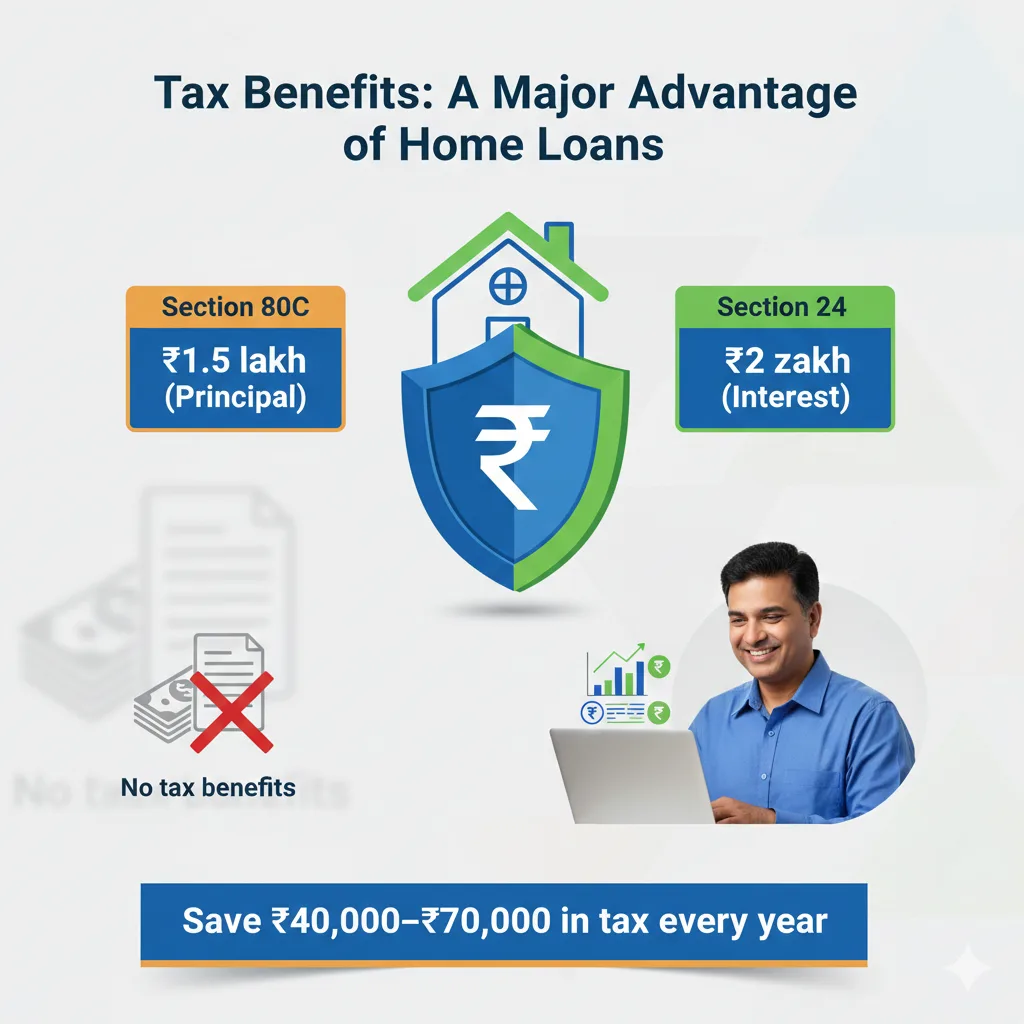

Tax Benefits: A Major Advantage of Home Loans

Home loans offer two key tax benefits:

- Section 80C: Up to ₹1.5 lakh on principal

- Section 24: Up to ₹2 lakh on interest

For a salaried person, this can save ₹40,000-₹70,000 in tax every year.

Personal loans offer no such tax relief (except in rare business or renovation cases).

Impact on Monthly Budget

- Home loans spread cost over decades

- EMIs stay manageable

- Personal loans compress repayment into a few years

- EMIs feel heavier

A ₹10 lakh personal loan can eat up a big chunk of your salary.

Credit Score and Approval

Banks assess:

- Income

- Employment stability

- Existing EMIs

- Credit score

Home loans require stronger profiles but are more forgiving once approved.

Personal loans are easier to get but can become expensive if you already carry debt.

Common Mistakes Borrowers Make

- Using personal loans for property purchase

- Ignoring total interest cost

- Overstretching EMI capacity

- Not comparing offers

- Mixing multiple personal loans

Borrowing should support goals, not strain your future.Real-Life Scenarios

Scenario 1: Buying a ₹50 lakh home

-> Home loan is the only sensible option.

Scenario 2: ₹1.5 lakh medical emergency

-> Personal loan fits better.

Scenario 3: Home renovation

-> Compare: home loan top-up vs personal loan.

What Regulators Advise

The Reserve Bank of India urges borrowers to:

- Understand total loan cost

- Read terms carefully

- Avoid over-borrowing

Official guidance is available at: https://www.rbi.org.in/

Conclusion

The choice between a home loan and a personal loan is not about which is “better”-it’s about what fits your purpose.

- For long-term, big goals -> Home loan

- For urgent, short-term needs -> Personal loan

Pick the right tool for the job. The wrong choice can cost you lakhs.

Written By Nakul

Disclaimer:

This article is for informational purposes only and does not constitute financial advice. Loan terms, rates, and eligibility vary by lender and may change. Always verify details with the bank and consult a qualified advisor before making borrowing decisions.

Reviewed for accuracy and last updated on January 31, 2026.