Mortgage vs Personal Loan: Key Differences Explained

When you find yourself in a situation where you require a substantial amount of money, you may consider two types of loans: a mortgage and a personal loan. While both types of loans allow you to borrow money, they are very different in terms of how they operate, and if you choose the wrong one, you could end up paying thousands of dollars.

A mortgage is designed for purchasing or refinancing a house. A personal loan is designed for flexibility, whether you are paying off medical expenses, consolidating debt, or financing a significant purchase.

While both types of loans are simply “loans,” they operate under different sets of rules, involve different levels of risk, and are used for entirely different purposes.

How This Comparison Helps Borrowers

This guide compares and contrasts mortgages and personal loans based on cost, risk, repayment terms, and practical applications. The purpose of this guide is to educate borrowers on which type of loan is best suited for which purpose, in order to avoid unnecessary expenses and loan errors.

What Is a Mortgage?

A mortgage is a long-term loan used to buy or refinance real estate.

Your home acts as collateral. That means if you stop making payments, the lender can take the property through foreclosure.

Because the loan is secured, mortgages usually offer:

- Lower interest rates

- Longer repayment terms

- Higher borrowing limits

Most U.S. mortgages run 15 to 30 years. Monthly payments are designed to be manageable over time, making homeownership possible for millions of Americans.

Mortgages are tightly regulated and often backed by government-sponsored entities like Fannie Mae and Freddie Mac.

What Is a Personal Loan?

A personal loan is typically unsecured. You don’t put up your house or car as collateral.

You can use it for almost anything:

- Medical bills

- Travel

- Moving expenses

- Home repairs

- Debt consolidation

Personal loans are short-term compared to mortgages, usually lasting between two and seven years.

Because they’re riskier for lenders, they usually come with:

- Higher interest rates

- Lower borrowing limits

- Faster approval times

They’re built for speed and flexibility-not for buying homes.

The Core Differences at a Glance

| Feature | Mortgage | Personal Loan |

|---|---|---|

| Purpose | Buy or refinance a home | Any major expense |

| Collateral | Home | Usually none |

| Term length | 15-30 years | 2-7 years |

| Interest rate | Lower | Higher |

| Loan size | Up to hundreds of thousands | Usually under $50,000 |

| Approval time | Weeks | Days or hours |

These differences exist for a reason. Each loan is optimized for a different financial need.

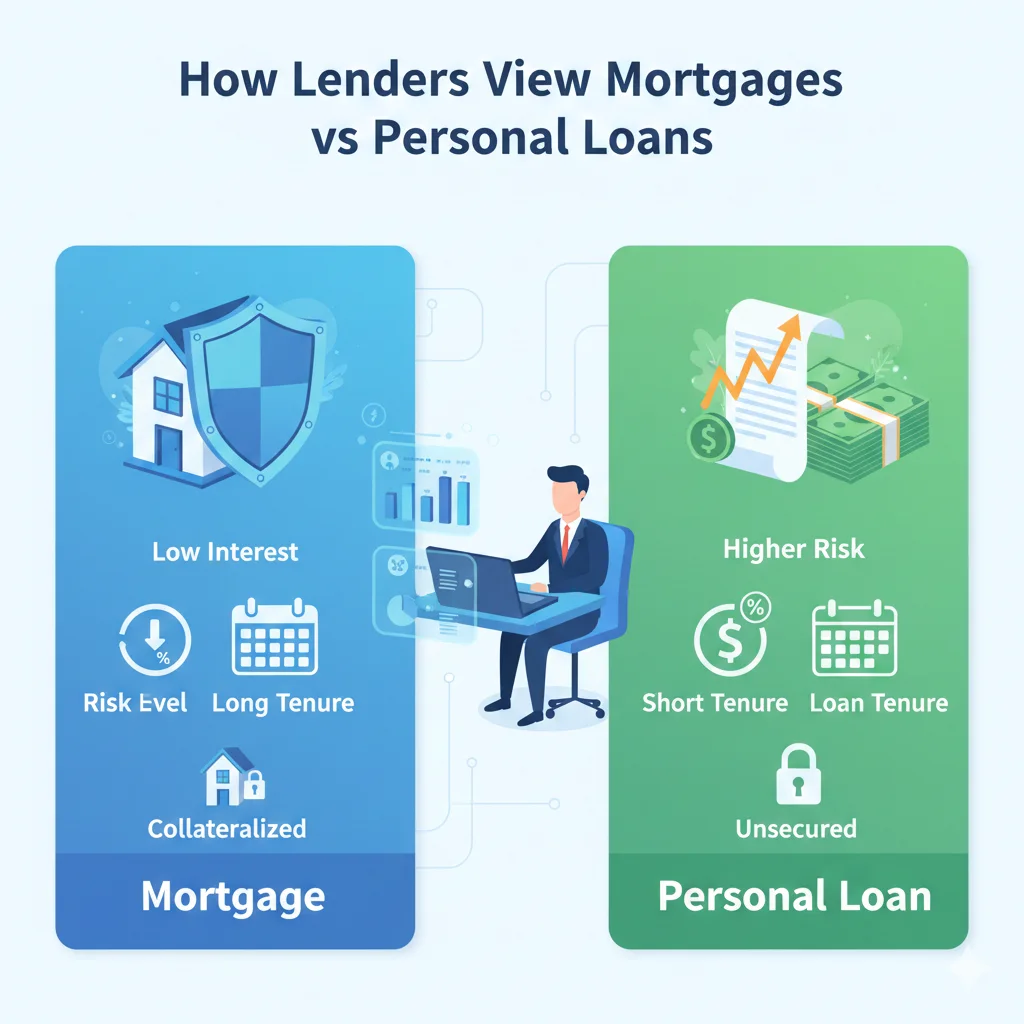

How Lenders View Mortgages vs Personal Loans

Because of risk, there is a big difference in how lenders treat mortgages and personal loans.

Mortgages are secured by property, which reduces lender risk and enables:

- Lower interest rates

- Longer repayment terms

- Larger loan amounts

Personal loans are often unsecured, so lenders offset risk by:

- Charging higher interest rates

- Limiting loan size

- Requiring stronger credit profiles

The big difference in risk is the primary reason for such a large difference in costs.

Interest Rates: The Biggest Cost Factor

Mortgages almost always carry lower interest rates than personal loans.

Why?

Because the lender can seize the home if you default. That security lowers risk.

In 2026, many U.S. mortgages still fall in the mid-to-high single digits, depending on market conditions and credit score. Personal loans often range from the high single digits to well over 20%.

That gap matters.

Borrow $30,000:

- Mortgage-style rate: You may pay a few thousand in interest

- Personal loan rate: You could pay double that

The same amount of money can cost wildly different totals depending on loan type.

Repayment Style and Monthly Impact

Mortgages spread payments over decades. That keeps monthly costs lower.

A $300,000 mortgage over 30 years can feel manageable. A $30,000 personal loan over three years can feel heavy.

Personal loans compress repayment. You pay more each month, but you’re done faster.

This difference shapes cash flow:

- Mortgages support long-term budgeting

- Personal loans demand short-term discipline

Neither is “better.” They simply serve different timelines.

When a Mortgage Makes Sense

A mortgage is the right tool when:

- You’re buying a home

- You’re refinancing an existing property

- You’re tapping home equity at low rates

Using a personal loan to buy a house rarely works. Loan limits are too low, and rates are too high.

Even for major renovations, homeowners often choose home equity loans or cash-out refinances instead of personal loans because of cost savings.

When a Personal Loan Makes Sense

A personal loan works best when:

- You need money quickly

- You don’t own property

- You’re covering a one-time expense

- You want predictable, short-term repayment

They’re common for:

- Emergency costs

- Medical bills

- Moving expenses

- Debt consolidation

They’re not ideal for large, long-term purchases like homes.

Risk and Consequences

The risk profiles are very different.

With a mortgage:

- Missed payments can lead to foreclosure

- You can lose your home

- Credit damage can be severe

With a personal loan:

- You won’t lose a house

- You may face collections

- Credit damage still occurs

Mortgages carry higher stakes. Personal loans carry higher costs.

Approval and Accessibility

Mortgages require:

- Extensive documentation

- Income verification

- Credit checks

- Property appraisals

Approval can take weeks.

Personal loans often require:

- Basic income proof

- Credit check

- Online application

Approval can happen within a day.

Speed is one of the biggest advantages of personal loans.

How Each Affects Your Credit

Both loans affect your credit score.

They influence:

- Payment history

- Credit mix

- Debt levels

Mortgages can improve credit over time because they demonstrate long-term responsibility. Personal loans can help too—if managed well.

Missed payments hurt both equally.

Real-World Example

You need $25,000.

Option 1: Personal loan at 18% for 5 years

- Monthly payment: ~$635

- Total interest: ~$13,000

Option 2: Home equity loan at 8% for 15 years

- Monthly payment: ~$239

- Total interest: ~$18,000

One is cheaper monthly. The other costs less overall.

The “right” choice depends on your cash flow and risk tolerance.

Regulatory Protections

Mortgages are heavily regulated. Borrowers receive disclosures, cooling-off periods, and federal protections.

Personal loans are simpler and less protected.

According to the Consumer Financial Protection Bureau (CFPB), mortgage rules are designed to ensure borrowers can reasonably repay and understand loan terms.

https://www.consumerfinance.gov

That level of oversight doesn’t exist for all personal loans.

Conclusion

Mortgages and personal loans are built for different purposes.

A mortgage is a long-term tool for owning property at lower cost.

A personal loan is a short-term solution for flexible spending.

One trades risk for affordability. The other trades speed for cost.

Understanding that trade-off helps you choose the right loan for the right moment-and avoid paying far more than you need to.

Written By Nakul

Disclaimer

This article is for informational purposes only and does not constitute financial or legal advice. Loan terms, rates, and eligibility vary by lender and individual credit profile. Always review official disclosures and consult a qualified financial professional before making borrowing decisions. Information is accurate to the best of our knowledge at the time of publication and may change.

Reviewed for accuracy and last updated on January 31, 2026.