Credit Card APR Explained: What It Really Costs

APR is one of the most significant pieces of information on your credit card, but it is also one of the most confusing.

APR is short for Annual Percentage Rate. It is the amount of interest you will pay on a balance in a year. If you are carrying a balance from month to month, APR determines how costly that balance will be.

A credit card with an APR of 24% is more than just “a little extra.” It can turn a $1,000 purchase into a $1,300 problem.

In 2026, with average U.S. credit card APRs hovering above 20%, understanding this number isn’t optional. It’s the difference between using credit as a tool and letting it quietly drain your money.

What Is Credit Card APR?

Credit card APR is the yearly cost of borrowing money on your card.

When you don’t pay your balance in full, your issuer charges interest. That interest is based on your APR.

Most cards show APR as a single percentage, such as:

- 19.99%

- 24.49%

- 29.99%

But in reality, APR works daily.

Your issuer divides your APR by 365 to get a daily rate, then applies it to your balance every day you carry debt.

That’s why interest grows faster than many people expect.

How APR Is Applied in Real Life

Let’s say your card has a 24% APR.

- Daily rate: about 0.066%

- Balance: $1,000

Each day, interest is added. After one month, you might owe around $20-$25 in interest alone.

If you only make the minimum payment, most of your money goes toward interest-not the original purchase.

That’s how a $1,000 balance can take years to eliminate.

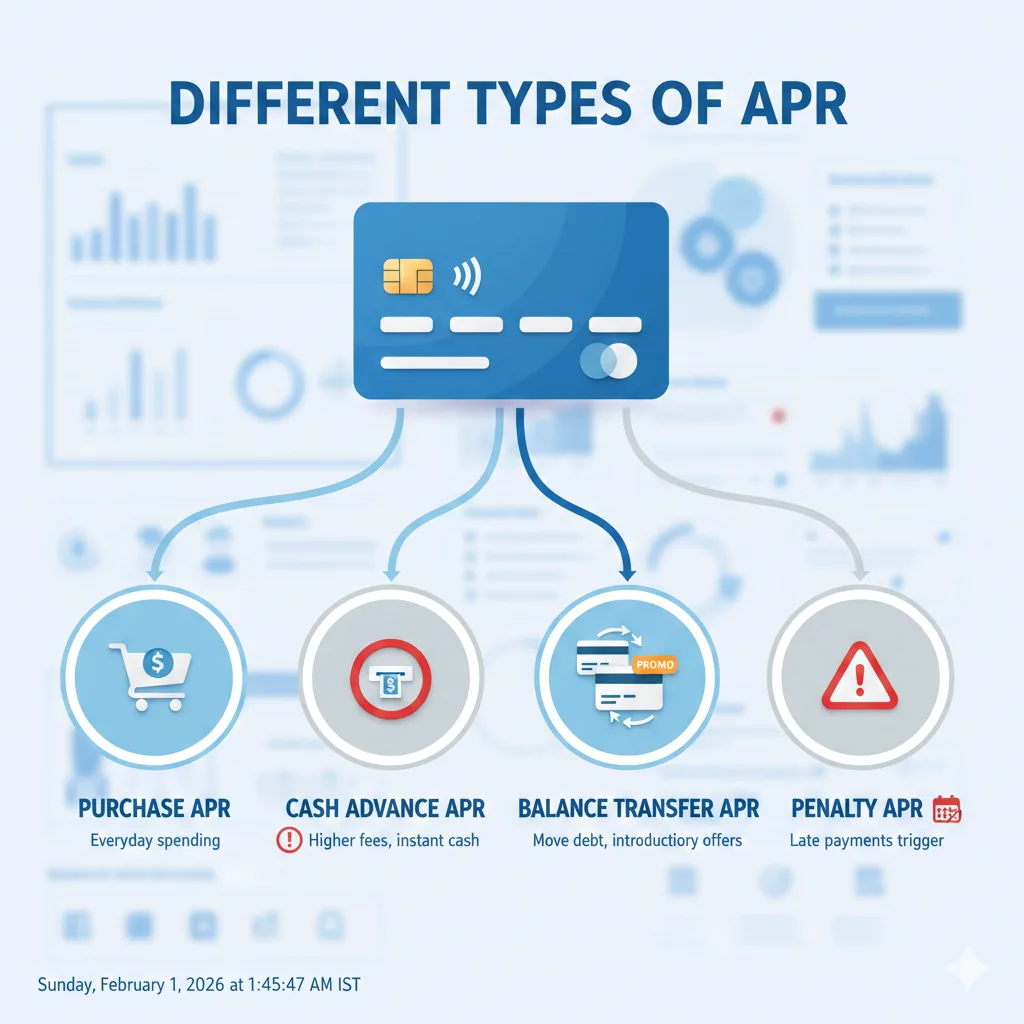

Different Types of APR

Credit cards often include multiple APRs:

- Purchase APR – For everyday spending

- Cash Advance APR – Usually higher

- Balance Transfer APR – Sometimes promotional

- Penalty APR – Applied after late payments

Cash advance APRs can exceed 30%. Penalty APRs can stay in effect for months.

That’s why reading the terms matters.

APR vs. Interest Rate

APR and interest rate are often used interchangeably, but APR is broader.

APR can include:

- Base interest rate

- Certain fees

- Promotional adjustments

For credit cards, APR mainly reflects the interest you’ll pay-but it’s still the clearest cost indicator.

Real Examples: How APR Changes the Cost

| Balance | APR | Interest in 1 Year* |

|---|---|---|

| $500 | 18% | ~$90 |

| $1,000 | 24% | ~$240 |

| $5,000 | 27% | ~$1,350 |

*Assumes no payments and simple illustration.

Now imagine making only minimum payments.

A $3,000 balance at 25% APR can take over 10 years to pay off and cost more than $2,000 in interest.

APR doesn’t just affect big purchases. It compounds.

Why APR Is So High in the U.S.

Credit card APRs in the U.S. are among the highest in the developed world.

Reasons include:

- Unsecured debt (no collateral)

- Higher default risk

- Federal interest rate changes

- Issuer profit models

When the Federal Reserve raises rates, card APRs often follow.

According to the Federal Reserve, average U.S. credit card APRs now exceed 20%, a historic high.

https://www.federalreserve.gov

This makes carrying a balance more expensive than ever.

When APR Doesn’t Matter

APR doesn’t affect you if:

- You pay your full balance every month

- You use a 0% promotional period correctly

In these cases, you avoid interest entirely.

That’s why many experts say the best strategy is simple:

Use credit cards for convenience, not borrowing.

How to Lower the Impact of APR

You can’t always change your APR, but you can reduce its effect:

- Pay balances in full

- Make more than the minimum

- Use 0% intro offers strategically

- Ask for a rate reduction

- Transfer high-interest balances

Even small extra payments reduce long-term interest dramatically.

Common APR Myths

“APR only matters for big purchases.”

Small balances grow too.

“Minimum payments are enough.”

They mostly feed interest.

“All cards charge the same.”

Rates vary widely by issuer and credit profile.

Written By Nakul

Disclaimer:

This article is for informational purposes only and does not constitute financial, legal, or professional advice. Credit card terms, APRs, and policies vary by issuer and individual credit profile and may change over time. Always review your card’s terms and conditions or consult a qualified financial professional before making decisions. Information is accurate to the best of our knowledge at the time of publication.

Reviewed for accuracy and last updated on February 1, 2026.